In the 1930s, the FHA refused to insure houses for Black families, or even insure houses in white neighborhoods that were too close to Black ones.

Updated: May 3, 2024 | Original: October 20, 2020

The Great Depression of the late 1920s and early 1930s delivered a gut punch to the average American. By 1933, a quarter of Americans were out of work, the national average income had slumped to less than half of what it had been a few years earlier and more than one million Americans faced foreclosure on their homes.

One of the multiple programs a newly-elected Franklin D. Roosevelt established to stimulate the economy offered home-buying aid for Americans—but only white Americans. The Federal Housing Administration operated through the New Deal’s National Housing Act of 1934 and promoted homeownership by providing federal backing of loans—guaranteeing mortgages. But from its inception, the FHA limited assistance to prospective white buyers.

Franklin D. Roosevelt's New Deal“The FHA had a manual which explicitly said that it was risky to make mortgage loans in predominantly Black areas,” explains Richard D. Kahlenberg, a senior fellow at The Century Foundation who has written about housing segregation in the United States. “And so as a result, the federal subsidy for home ownership went almost entirely to white people.”

The assistance program not only limited recipients to white Americans, it established and then reinforced housing segregation in the United States, effectively drawing lines between white and Black neighborhoods that would persist for generations.

For example, in 1940, the FHA denied insurance to a private builder in Detroit because he intended to construct a housing development near a predominantly Black neighborhood. The FHA only wanted to insure houses in white neighborhoods.

The builder responded by constructing a half-mile long, six-foot high concrete wall between the Black neighborhood and where he planned to build, recounts historian Richard Rothstein in The Color of Law: A Forgotten History of How Our Government Segregated America. Assured that this wall would keep the neighborhoods racially segregated, the FHA then agreed to insure the houses.

The FHA not only focused its assistance on prospective white homeowners, its policies actively sought to insure mortgages in white neighborhoods that would remain white.

“If a [Black] family could afford to buy into a white neighborhood without government help, the FHA would refuse to insure future mortgages even to whites in that neighborhood, because it was now threatened with integration,” Rothstein writes in The American Prospect.

Many housing deeds stated outright that a house could only be sold to white people, explaining this was in accordance with FHA requirements. William Levitt, who developed the Levittown suburban communities for returning World War II veterans, complied with the FHA by only selling to white veterans and creating deeds that prohibited them from reselling their homes to Black Americans.

Social Security differed from other New Deal programs in that it wasn’t a short‑term solution to the Great Depression. It was a long‑term investment.

The Hoover Dam, LaGuardia Airport and the Bay Bridge were all part of FDR's New Deal investment.

About 8,500 women attended the camps inspired by the CCC and organized by Eleanor Roosevelt—but the "She‑She‑She" program was mocked and eventually abandoned.

Like the Detroit builder, developers also tried to make their housing projects seem “less risky” by using barriers to separate them from predominantly Black neighborhoods. One common barrier, Kahlenberg says, became highways, which still separate many predominantly white and predominantly Black neighborhoods today.

In addition to the FHA’s discriminatory practices, federal housing projects from the 1930s onward helped keep Black Americans in neighborhoods with fewer education and job opportunities than white neighborhoods.

“The existing patterns of segregation were carefully and deliberately engineered—socially engineered—by the government in the first place,” says Kahlenberg.

The Fair Housing Act of 1968 sought to end these discriminatory practices but didn’t completely end federal redlining—the denial of services like loans based on race—or address the negative effects that decades of discrimination and segregation had already had on Black Americans.

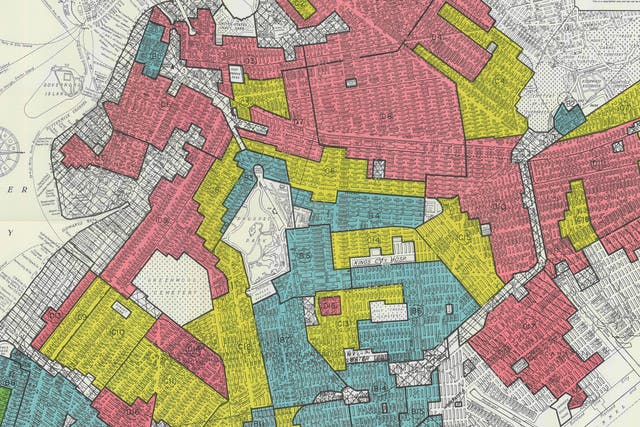

The term “redlining” originates with actual red lines on maps that identified predominantly-Black neighborhoods as “hazardous.” Starting in the 1930s, the government-sponsored Home Owners’ Loan Corporation and the Federal Home Loan Bank Board used these maps to deny lending and investment services to Black Americans.

This lack of investment had a profound, lasting impact on Black neighborhoods, says Halley Potter, a senior fellow at The Century Foundation. “We see the legacy today when you look at maps and housing values and demographic patterns in our cities."